Commercial Property Value Calculator

Enter values and click calculate to see results

You look at a warehouse in the industrial district or a retail strip mall on the corner. The listing says it generates $150,000 a year in rent. Does that mean the building is worth $150,000? Definitely not. In fact, it’s probably worth significantly more. But how much more? And why?

If you are looking to buy commercial real estate in 2026, understanding the math behind the price tag is non-negotiable. Unlike residential homes, where emotions and 'curb appeal' often drive prices, commercial property values are cold, hard calculations based on income potential. If you cannot calculate the value yourself, you are leaving money on the table-or worse, overpaying for a liability.

The core metric you need to master is the relationship between Net Operating Income and the Capitalization Rate. This formula is the heartbeat of commercial real estate valuation. It strips away the fluff and tells you exactly what an asset is worth based on its ability to generate cash flow. Let’s break down how to do this accurately, step-by-step.

Understanding Net Operating Income (NOI)

Before you can value a property, you must determine its true earning power. Many beginners make the mistake of taking the gross rent collected and calling it a day. That is dangerous. Gross income includes vacancies, bad debts, and maintenance costs that eat into your profit.

To get your NOI, start with the Gross Potential Income (GPI). This is the total rent you would collect if every unit was occupied 100% of the time at market rates. From there, subtract:

- Vacancy and Credit Losses: No building is ever 100% occupied forever. In Adelaide’s current market, a conservative estimate for vacancy might be 5-8% depending on the asset class.

- Operating Expenses: This includes property management fees, insurance, repairs, utilities (if paid by the landlord), landscaping, and security.

- Property Taxes: These are operating costs. Do not confuse them with mortgage payments.

Crucially, you do not subtract mortgage payments, principal repayments, or income tax from NOI. Why? Because NOI measures the performance of the building itself*, independent of how you finance it. Whether you pay cash or take a loan, the building produces the same income. By removing debt from the equation, you create a standardized number that allows you to compare a fully paid-off office block against a leveraged retail center.

For example, if a shopping center brings in $500,000 in rent but has $150,000 in expenses (including taxes and maintenance), the NOI is $350,000. This $350,000 is the engine that drives the valuation.

The Capitalization Rate (Cap Rate): The Market's Pulse

Now that you have the NOI, you need a multiplier. That multiplier is the Capitalization Rate, or Cap Rate. Think of the Cap Rate as the expected rate of return on an all-cash purchase. It reflects the risk associated with the property type and location.

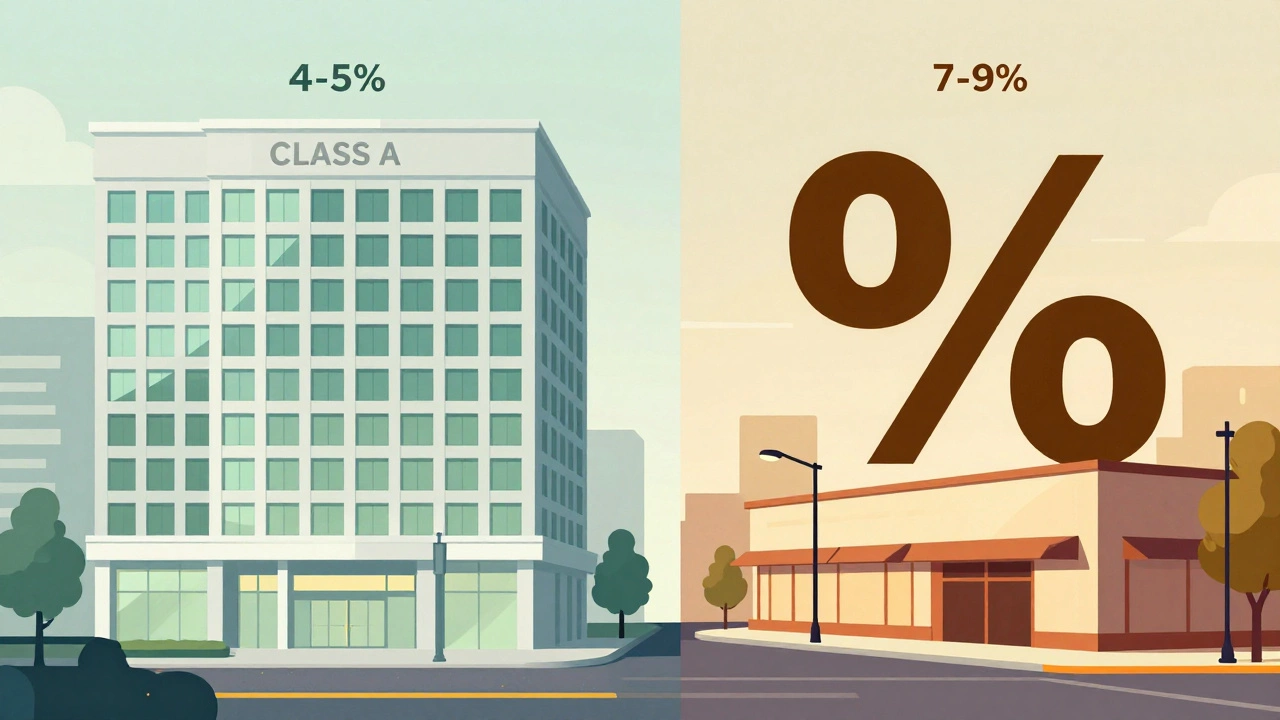

In 2026, interest rates have stabilized compared to the volatility of previous years, which has shifted Cap Rates across different sectors. Generally, lower-risk properties like Class A office buildings in prime CBD locations will have lower Cap Rates (perhaps 4-5%), because investors accept lower returns for safety. Higher-risk assets, such as older retail stores in declining suburbs or specialized industrial warehouses with single tenants, will command higher Cap Rates (7-9% or more) to compensate for the increased chance of vacancy or tenant default.

Where do you find the right Cap Rate? You don't guess. You look at recent sales of comparable properties ('comps') in the same area. If similar warehouses in your target suburb sold at a 6% Cap Rate last quarter, that is your benchmark. Using a generic national average is a recipe for error. Local market dynamics dictate the rate.

The Valuation Formula: Putting It Together the Puzzle

The actual calculation is surprisingly simple. The complexity lies in getting the inputs right. The formula is:

Property Value = Net Operating Income (NOI) / Capitalization Rate

Let’s walk through a concrete scenario. Imagine you are eyeing a medical center in Glenelg. The seller provides financial statements showing:

- Gross Rent: $600,000

- Vacancy Loss (estimated 5%): -$30,000

- Operating Expenses (management, insurance, repairs): -$120,000

- Property Taxes: -$40,000

Your NOI is $600,000 - $30,000 - $120,000 - $40,000 = $410,000.

You research recent sales of similar medical facilities in the region and find they transacted at a Cap Rate of 6.5%. Plugging this into the formula:

$410,000 / 0.065 = $6,307,692.

This suggests the fair market value of the property is approximately $6.3 million. If the asking price is $7 million, the deal doesn’t make sense unless you can increase the NOI or believe Cap Rates will drop further. If the asking price is $5.5 million, you might be looking at a bargain, assuming the numbers are accurate.

Common Pitfalls in Calculating Property Value

Even with the correct formula, many investors trip up on the details. Here are the most frequent errors I see in the field:

- Ignoring Lease Expirations: A high NOI today means little if the major tenant leaves next month. Always adjust the NOI to reflect 'stabilized' income-what the property will earn once leases renew at market rates. If a lease is below market, factor in the cost of re-leasing (tenant improvements, free rent periods).

- Miscalculating Expenses: Sellers often present 'best-case' expense scenarios. They might exclude major roof replacements or HVAC upgrades from their operating expenses. Always add a contingency reserve (e.g., 5-10% of gross income) for capital expenditures (CapEx) when estimating true long-term NOI.

- Using the Wrong Cap Rate: Applying a low-risk office Cap Rate to a high-risk retail property inflates the value artificially. Always match the Cap Rate to the specific risk profile of the asset class and tenant quality.

- Confusing Cash-on-Cash Return with Cap Rate: Cash-on-Cash return considers your mortgage payments and down payment. Cap Rate does not. Never use Cash-on-Cash to determine property value; use it only to evaluate financing efficiency.

Comparing Valuation Methods: When to Use What

While the Income Approach (NOI/Cap Rate) is the gold standard for income-producing properties, it isn't the only tool. Understanding when to use other methods helps validate your numbers.

| Method | Best Used For | Key Metric | Limitations |

|---|---|---|---|

| Income Approach | Retail, Office, Industrial, Multi-family | NOI & Cap Rate | Relies heavily on accurate expense data |

| Sales Comparison | Land, Unique Properties, Small Buildings | Price per Square Foot | Few comparable sales may exist |

| Cost Approach | New Construction, Special Purpose (Schools, Churches) | Replacement Cost minus Depreciation | Does not account for market demand/income |

For most commercial investments, the Income Approach is primary. However, cross-checking with the Sales Comparison method (looking at price per square foot of recent sales) can highlight discrepancies. If your calculated value is $6 million, but similar buildings sold for $1,000 per square foot (and this building is 5,000 sq ft, implying a $5 million value), you need to investigate why your income projection differs from the market reality.

Impact of Interest Rates on Valuation in 2026

The macroeconomic environment plays a huge role in Cap Rates. In 2026, after years of fluctuating central bank policies, investors are more sensitive to the spread between borrowing costs and property yields. When interest rates rise, Cap Rates typically expand (go up), which lowers property values. Conversely, if rates stabilize or fall, Cap Rates compress (go down), boosting values.

As a buyer, you must assess whether current Cap Rates adequately compensate you for the cost of capital. If you can borrow at 6%, buying a property with a 6.5% Cap Rate leaves very little margin for error. A small increase in expenses or a slight vacancy could turn your positive cash flow negative. Smart investors in 2026 are looking for properties with strong, long-term leases and inflation-linked rent escalators to protect against these economic shifts.

Practical Steps to Verify Seller's Numbers

Never trust the pro forma provided by the seller without verification. Here is your checklist:

- Request T12 Statements: Ask for the trailing twelve months of bank statements and profit/loss reports. Compare these against the tax returns filed.

- Review Lease Abstracts: Get a summary of every lease, including expiration dates, rent escalation clauses, and renewal options. Look for 'below-market' rents that are about to reset.

- Inspect Physical Condition: Hire a qualified building inspector. Hidden structural issues can lead to massive unexpected expenses that destroy your NOI.

- Analyze Tenant Creditworthiness: A property with one national chain tenant is less risky than one with five small local businesses. Check the financial health of major tenants.

Valuing commercial property is less about guessing and more about rigorous due diligence. The formula is simple, but the accuracy of your inputs determines your success. By mastering NOI calculation and understanding local Cap Rate trends, you move from being a hopeful buyer to a sophisticated investor who knows exactly what they are paying for.

What is a good Cap Rate for commercial property in 2026?

There is no single 'good' Cap Rate, as it depends on risk and asset class. In 2026, stable Class A office properties might trade at 4-6%, while riskier retail or older industrial assets may range from 7-9% or higher. A 'good' rate is one that exceeds your cost of capital and provides a sufficient risk premium for your investment goals.

Does mortgage payment affect the property value calculation?

No. Mortgage payments are excluded from the Net Operating Income (NOI) calculation. Property value is determined by the income the building generates regardless of how it is financed. Mortgage payments affect your personal cash flow and Cash-on-Cash return, but not the intrinsic market value of the asset.

How do I find the Net Operating Income (NOI)?

Calculate NOI by taking the Gross Potential Income, subtracting vacancy and credit losses, and then deducting all operating expenses (property management, insurance, repairs, utilities, and property taxes). Do not include mortgage payments, depreciation, or income taxes in this calculation.

Why is the Income Approach preferred for commercial real estate?

The Income Approach is preferred because commercial properties are purchased primarily for their income-generating potential. Buyers invest to receive a return on their capital. Therefore, the value is directly tied to the net income the property produces, making NOI and Cap Rate the most relevant metrics for valuation.

What happens to property value if Cap Rates go up?

If Cap Rates go up, property values go down, assuming NOI remains constant. This inverse relationship exists because a higher Cap Rate implies investors require a higher return for perceived risk, which reduces the amount they are willing to pay for the same stream of income.