Rental Property Profit Calculator

Results

When you buy a rental property, you’re not just buying bricks and mortar-you’re buying a business. And like any business, you need to know what a healthy profit looks like. Too little, and you’re working for free. Too much, and you’ll struggle to find tenants. So how much profit should you actually make? The answer isn’t one number. It’s a range, shaped by location, costs, and your goals.

Start with the basics: rental yield

Rental yield tells you what percentage of your property’s value you’re earning in rent each year. It’s the most basic measure of profitability. You calculate it like this: annual rent divided by property value, multiplied by 100.

For example, if you buy a property for $500,000 and rent it out for $500 a week, that’s $26,000 a year. Your gross yield is 5.2%. That’s solid in most Australian cities. But gross yield doesn’t tell the whole story. It ignores all your expenses.

Net yield is what matters. That’s your profit after mortgage payments, property management fees, council rates, insurance, repairs, and vacancies. In Adelaide, a typical net yield for a well-managed rental sits between 4% and 6%. If you’re getting less than 3.5%, you’re likely overpaying or undercharging.

What’s a realistic profit after all costs?

Let’s say you buy a two-bedroom unit in Adelaide for $480,000 with a 20% deposit. Your mortgage is $384,000 at 6.5% interest. Your weekly rent is $480. That’s $24,960 a year in rent.

Now subtract the costs:

- Mortgage interest: ~$25,000/year (at 6.5%)

- Property management (8% of rent): $2,000/year

- Insurance: $1,200/year

- Council rates and water: $2,000/year

- Maintenance and repairs: $1,500/year

- Vacancy (4 weeks/year): ~$1,800

Total expenses: ~$33,500

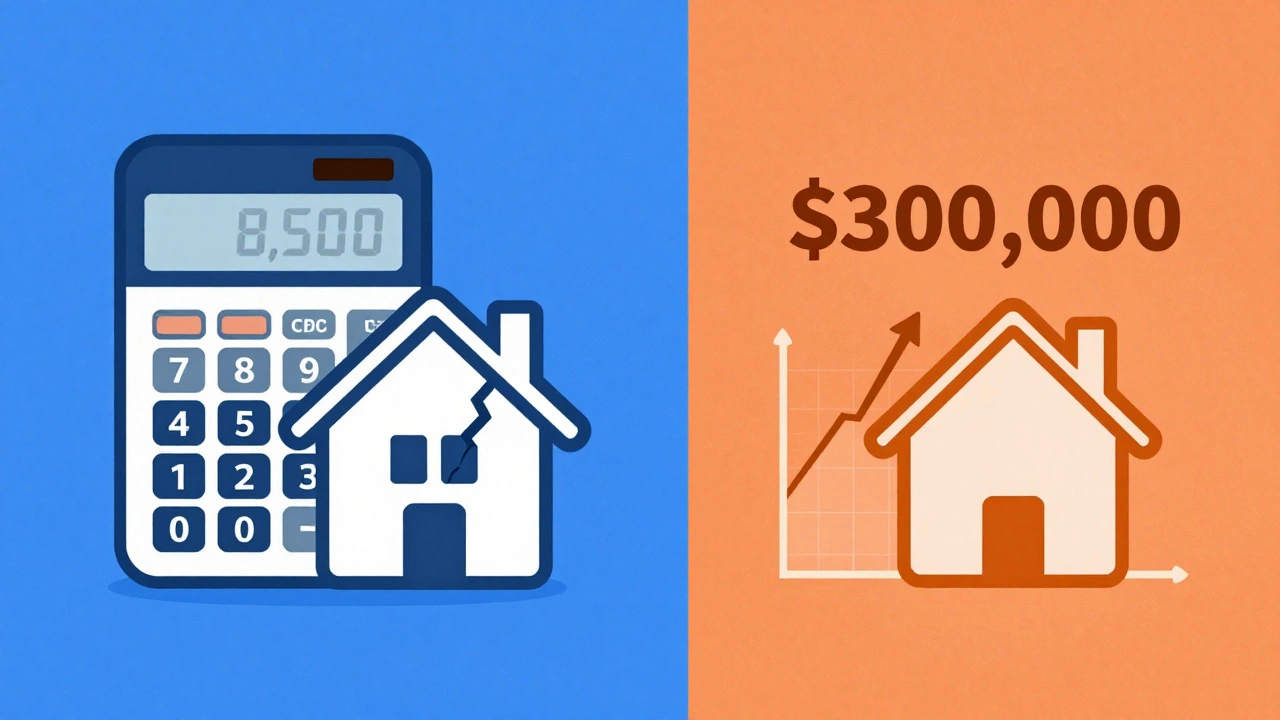

That means you’re losing $8,500 a year before tax. Sounds bad? Maybe. But you’re still building equity. And you’re getting tax deductions on almost all of those costs. Your cash flow might be negative, but your long-term wealth is growing.

Now flip it. Buy the same unit for $380,000 with the same rent. Mortgage drops to $304,000. Interest is now ~$19,800. Total costs fall to ~$27,300. Your net cash flow is now +$2,660 a year. That’s a $220 a month profit. Not life-changing, but it’s passive income with zero effort.

Location changes everything

Adelaide isn’t Melbourne or Sydney. You won’t get 8% yields here. But you also won’t get $1,200-a-week rents that come with 40% vacancy rates. Adelaide offers stability. Tenants stay longer. Properties don’t crash. That’s worth something.

Look at the suburbs. A three-bedroom house in Morphett Vale or Noarlunga Centre might rent for $550 a week and cost $420,000. That’s a 6.5% gross yield. With lower property management fees (many landlords self-manage here), net yield hits 5.5%. That’s better than most city apartments.

Meanwhile, a studio in the CBD might rent for $450 but cost $520,000. Gross yield: 4.3%. Net yield: maybe 2.8% after fees and strata. You’re not making profit-you’re paying to play.

Profit isn’t just cash flow

Many investors forget that profit isn’t just what lands in your bank account. It’s also equity growth. If your property rises 5% a year in value, that’s $24,000 in Adelaide on a $480,000 home. That’s profit you can’t spend today-but it’s real wealth.

Over 10 years, a 5% annual increase turns $480,000 into $780,000. Even if you broke even on cash flow, you’ve made $300,000 in equity. That’s the real game.

Think of it this way: you’re not trying to make $1,000 a month from rent. You’re trying to build a $1 million property portfolio over 15 years. Each property adds $50,000-$100,000 in equity per year. That’s the profit.

What’s a good target?

Here’s a simple rule: aim for a net yield of at least 4.5% after all costs. If you’re below that, ask why. Is the price too high? Are you overpaying for management? Is the rent too low?

But don’t chase high yields blindly. A 7% yield in a rundown suburb with high turnover and crime might cost you $10,000 a year in repairs and lost rent. That’s not profit-it’s a headache.

Look for balance. A 5% net yield in a stable, family-friendly suburb with low vacancy and rising demand is better than a 6% yield in a volatile area. Tenants who stay three years save you $3,000 in re-leasing costs alone.

How to improve your profit

You can’t control the market, but you can control your costs and your rent.

- Self-manage: If you’re comfortable with maintenance and screening, skip the agent. Save 8% of rent.

- Upgrade smartly: A new kitchen or bathroom can boost rent by $50-$100/week. That’s $600-$1,200 extra a year. Payback under 2 years.

- Review rent annually: Don’t wait for the market to push you. Check what similar properties are renting for. A $25/week increase is $1,300 extra a year.

- Use a mortgage broker: A 0.5% lower interest rate on a $400,000 loan saves you $2,000 a year.

- Claim every deduction: Depreciation, interest, travel, accounting fees-all deductible. Get a quantity surveyor’s report. It’s worth $1,000+ in tax savings.

When to walk away

Some properties just don’t make sense. If you’re consistently losing $500 a month after tax, and the market isn’t rising, it’s time to reconsider. Holding onto a bad investment because you “don’t want to sell at a loss” is a trap. The loss is already there-in your bank account.

Ask yourself: if I didn’t own this property today, would I buy it now at this price and rent level? If the answer is no, it’s not an investment. It’s a liability.

Bottom line

You should aim for at least a 4.5% net rental yield in Adelaide. That means $200-$400 a month profit after all costs on a typical property. Anything less needs fixing. Anything more is a bonus.

But profit isn’t just cash. It’s equity. It’s stability. It’s building something that outlives you. The best rental properties don’t make you rich overnight. They make you secure over time.

If you’re buying now, focus on location, cash flow, and long-term growth-not just the rent. The profit will follow.

What’s a good rental yield in Adelaide in 2025?

A good gross rental yield in Adelaide is between 5% and 6%. After all expenses-mortgage, management, rates, insurance, and repairs-a net yield of 4.5% to 5.5% is realistic for well-maintained properties in stable suburbs. Anything below 4% usually means you’re overpaying or undercharging.

Is negative gearing worth it for rental property?

Negative gearing-where your rental costs more than it earns-can be worth it if you’re focused on long-term capital growth and tax benefits. In Adelaide, many investors break even or lose $100-$300 a month but gain $10,000-$20,000 in equity annually from property growth. Tax deductions on interest, repairs, and depreciation often offset most of the loss. It’s a strategy for wealth building, not monthly income.

How much should I charge for rent?

Check recent rentals on realestate.com.au for similar properties in the same street or suburb. In Adelaide, a two-bedroom house in a good location rents for $450-$550 a week. Don’t overprice-vacancies cost more than a small rent cut. A $25 weekly increase can be justified with minor upgrades like new flooring or a fresh paint job.

Should I use a property manager?

If you’re busy, live far away, or dislike dealing with tenants, yes. But in Adelaide, many landlords self-manage successfully. Property managers typically charge 8% of rent plus GST. That’s $40 a week on a $500 rent. If you’re comfortable handling repairs, screening, and leases, you can save $2,000 a year. Just be ready to respond quickly to emergencies.

Can I make a profit on a low-budget rental?

Yes, but it’s harder. A $300,000 property with $400 rent might give you a 6% gross yield, but high maintenance and tenant turnover can eat into profits. Focus on suburbs with low vacancy and stable demand. Avoid properties needing major repairs unless you can do the work yourself. The key is buying below market value and keeping costs tight.

How does inflation affect rental profits?

Inflation helps rental investors. Rents tend to rise with inflation, while your mortgage payment stays fixed. If your rent goes up 3% a year and your mortgage is locked in, your profit margin grows. Plus, property values usually rise with inflation. This is why real estate is a classic inflation hedge.

Next steps if you’re ready to buy

- Run the numbers on 5-10 properties you’re considering. Use a rental calculator to estimate net yield.

- Visit the suburb at different times of day. Talk to local real estate agents. Ask about vacancy rates and tenant types.

- Get a pre-approval from a mortgage broker who knows investment loans.

- Don’t rush. Wait for the right property at the right price. One good deal beats five mediocre ones.