Capital Gains Tax Calculator for Australian Non-Residents

How This Works

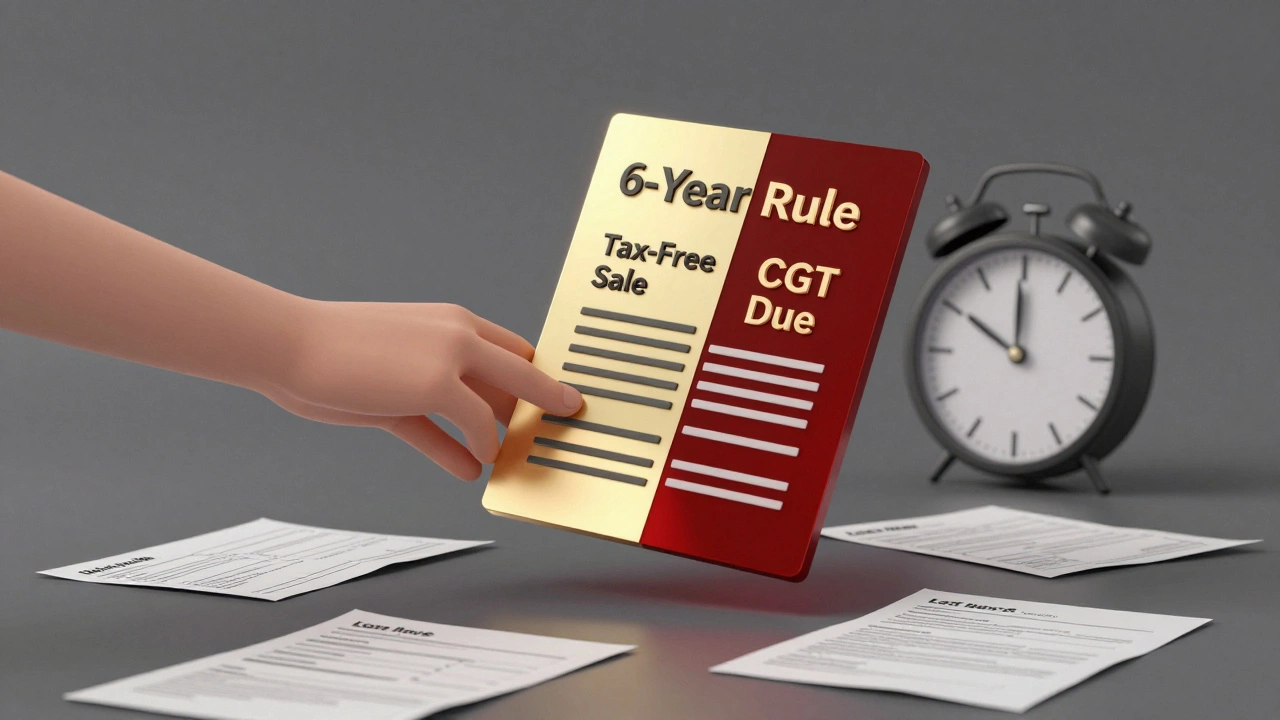

Calculates taxable gains based on Australia's 6-year rule. The portion of the gain from when you moved out is taxable to non-residents.

Key Information

Based on your inputs, you could save up to in capital gains tax by selling within the 6-year window.

Tax Calculation Breakdown

- The 6-year rule only applies if you lived in the property as your main residence before moving out.

- Rental income during your absence does not break the rule.

- You must sell within 6 years of moving out (no extensions).

- If you return to live in the property, you can reset the 6-year clock.

- All sales must be reported to the ATO, even if no tax is due.

When you own property in Australia but don’t live here, the 6-year rule can save you thousands in capital gains tax - if you know how to use it. This rule isn’t a loophole. It’s a legal part of Australia’s tax code, designed for people who leave the country but still hold onto their home. Many non-residents don’t even know it exists. Others misuse it and end up with a surprise tax bill. Here’s how it actually works, what you need to do, and what happens if you get it wrong.

What the 6-Year Rule Actually Means

The 6-year rule lets you treat your former main residence as if it’s still your main home - even after you’ve moved out and become a non-resident for tax purposes. This means you can sell it later without paying capital gains tax (CGT), as long as you sell within six years of moving out.

Let’s say you lived in your Melbourne apartment for three years, then moved to Canada for work. You kept the apartment, rented it out, and didn’t buy another home in Australia. If you sell that apartment within six years of leaving, you pay zero CGT. If you sell after six years and one day? You owe tax on the full profit.

This rule applies only if you were an Australian tax resident when you first moved out. If you were never a resident - say, you bought the property as a foreign investor - the rule doesn’t apply. You’re not eligible.

Who Can Use the 6-Year Rule?

You qualify if:

- You owned the property as your main residence before leaving Australia

- You were an Australian tax resident at the time you moved out

- You didn’t nominate another property as your main residence while overseas

- You sell the property within six years of moving out

It doesn’t matter if you rented it out. You can have tenants, collect rent, and still be covered. The rule doesn’t care if the property was generating income. What matters is your connection to it as your home before you left.

Here’s a real case: A Sydney couple bought a house in 2018, lived there for two years, then moved to Singapore for work. They rented out the house. In 2025, they sold it. Because they sold within six years of moving out - and never claimed another home as their main residence - they paid no capital gains tax. The Australian Taxation Office (ATO) accepted their claim.

What Happens If You Go Over Six Years?

If you sell after the six-year window, the rule disappears. You’ll owe CGT on the full gain from the time you became a non-resident.

Let’s say you moved out in January 2020 and sold in July 2027. That’s seven years and six months. The ATO will calculate your capital gain from January 2020 onward. Any increase in value before you left is still tax-free - but everything after that point is taxable.

There’s no grace period. No exceptions. No appeals. The six-year limit is strict. Even if you had a medical emergency, job loss, or family crisis, the clock doesn’t pause. You need to plan ahead.

Can You Reset the Clock?

Yes - but only once.

If you move back into the property as your main residence before the six years are up, you reset the clock. The six-year period starts again from the day you move out the second time.

For example: You move out in 2021, rent it out, then move back in 2024. You live there for 18 months, then move overseas again in 2026. Now you have a new six-year window from 2026. You could sell in 2032 without CGT.

This reset only works if you lived in the property as your main residence after returning. You can’t just move back for a week and claim it. You need to prove you re-established it as your home - mail, bills, voter registration, school enrolment, etc.

What About Multiple Properties?

You can only have one main residence at a time. If you own two homes and move out of one to live in the other, you can’t apply the 6-year rule to both.

Let’s say you owned a house in Perth and bought a unit in Brisbane. You lived in the Perth house for five years, then moved into the Brisbane unit. If you sell the Perth house after moving out, the 6-year rule still applies - but only if you didn’t nominate the Brisbane unit as your new main residence. If you did, the Perth house loses its main residence status from the day you moved in.

The ATO doesn’t guess. They look at your tax returns, bank statements, driver’s license address, and utility bills. If your records show you’re living somewhere else, that’s your new main residence.

Common Mistakes People Make

Here are the top three errors:

- Thinking the rule applies to any property - It only works if you lived in it first. Buying a property as an investment from day one? No exemption.

- Assuming renting it out breaks the rule - It doesn’t. You can rent it for six years and still be covered.

- Forgetting to report the sale - Even if you owe no tax, you still need to declare the sale on your Australian tax return. The ATO has access to property records. If you don’t report it, they’ll come after you.

Another big one: people assume the rule applies to inherited property. It doesn’t. If you inherited a house and never lived in it, you’re treated as a non-resident investor from day one. No 6-year exemption.

How to Prove You Qualify

The ATO doesn’t ask for paperwork upfront. But if they audit you - and they will if you sell for a big profit - you need to prove you met the conditions.

Keep these records:

- Proof you lived there (rates notices, utility bills, bank statements with your address)

- Proof you were an Australian tax resident when you left (tax returns, visa status)

- Proof you didn’t nominate another home as your main residence (no other property claimed as main residence on tax returns)

- Proof of move-out date (lease termination, forwarding address, employment contract ending)

Don’t wait until the sale to gather this. Start now. Store digital copies. Back them up. The ATO can look back up to five years - but if they suspect fraud, they can go further.

What If You’re Not an Australian Citizen?

It doesn’t matter. Citizenship is irrelevant. What matters is your tax residency status.

If you were a tax resident of Australia - even if you’re a New Zealander, American, or Indian citizen - and you lived in the property as your main home, you’re eligible.

If you bought the property as a foreigner, never lived there, and never paid Australian tax on income - you’re not eligible. The rule is for people who had a life here, not investors.

What Happens If You Sell After the 6-Year Window?

You’ll pay CGT on the portion of the gain that happened after you became a non-resident.

Example: You bought a house for $500,000 in 2017. You lived there until 2021. You moved out and became a non-resident. The house was worth $700,000 then. You sold it in 2026 for $900,000.

The gain before you left: $200,000 (tax-free).

The gain after you left: $200,000 (taxable).

You owe CGT on $200,000. If you’re a non-resident, you pay 32.5% on that gain - unless you’re from a country with a tax treaty that reduces it.

That’s $65,000 in tax. The 6-year rule could have saved you every dollar.

Final Advice

If you own property in Australia and plan to leave - or have already left - check the date you moved out. Write it down. Mark the six-year deadline on your calendar. If you’re close to that date and haven’t sold, consider holding off if you can. Or, if you’re thinking of returning, moving back in for even a few months could reset the clock.

Don’t rely on advice from real estate agents or accountants who don’t specialize in cross-border tax. Talk to a tax advisor who handles non-residents. The ATO doesn’t care how much you earn. They care about the dates. And they’re watching.

Does the 6-year rule apply to inherited property?

No. The 6-year rule only applies if you lived in the property as your main residence before becoming a non-resident. If you inherited a property and never lived in it, you’re treated as a foreign investor from the moment you acquired it. You won’t qualify for the exemption, even if you later move in.

Can I use the 6-year rule if I rent out my home while overseas?

Yes. Renting out your former home doesn’t break the rule. You can have tenants, collect rent, and still qualify for the capital gains tax exemption as long as you sell within six years of moving out and didn’t nominate another property as your main residence.

What if I move back to Australia before the six years are up?

Moving back in resets the clock. If you live in the property as your main residence again, the six-year period starts over from the date you leave the second time. You need to prove you re-established it as your home - with documents like utility bills, bank statements, and tax returns showing your address.

Does the 6-year rule apply to non-citizens?

Yes - if you were an Australian tax resident when you lived in the property. Citizenship doesn’t matter. What matters is your residency status at the time you moved out. If you were paying Australian tax and claimed the property as your main home, you qualify - even if you’re a U.S. or UK citizen.

Do I need to declare the sale if I owe no tax?

Yes. Even if you qualify for the exemption and owe no capital gains tax, you must still report the sale on your Australian tax return. The ATO receives property sale data from state land registries. Failing to report it can trigger an audit, even if you’re not liable for tax.